Mortgage Compliance & Its Impact on Bank Technology

At no other time have regulations played such an important role in the mortgage industry. Banks and credit unions are encountering a new regulatory framework; improved technology and automated solutions are increasingly necessary to maintain compliance. Prior to the credit crisis, mortgage regulations had focused mainly on the originations sector, but this is rapidly changing as regulators give the servicing sector more attention.

The full outcomes from the implementation of Dodd-Frank are only starting to have an impact. The mortgage and real estate industries are particularly impacted by three specific titles of Dodd-Frank:

- Title IX: Investor Protections and Improvements to the Regulation of Securities

- Title X: the Consumer Financial Protection Bureau (CFPB)

- Title XIV: the Mortgage Reform and Anti-Predatory Lending Act

[For more on regulation and technology in banking: Regulation: the Mother of Invention?]

Perhaps most visible is the CFPB as it begins to review copies of monthly statements, consumer payment records, and bills from vendors documenting services related to loan accounts. The following compliance requirements, policies, and procedures are all subject to CFPB audit and enforcement.

- Periodic billing statements

- Adjustable-rate mortgage interest rate adjustment notices

- Prompt payment crediting and payoff payments

- Force-placed insurance

- Error resolution and information requests

- Information management policies and procedures

- Early intervention with delinquent borrowers

- Continuity of contact with delinquent borrowers

- Loss mitigation procedures

(Source: Accenture, "The Rising Cost of Mortgage Loan Servicing," April 28, 2014.)

The agency has also been given responsibilities under Title X of Dodd-Frank that were previously held by other authorities. This includes several mortgage servicing provisions. For instance, Regulation C, which implements the Home Mortgage Disclosure Act, had fallen under the purview of the Federal Reserve Board. It is now enforced by the CFPB. That agency is amending other rules, such as Regulation X of the Real Estate Settlement Procedures Act and Regulation Z as it relates to the Truth in Lending Act. Appraisal management companies (AMCs) are being impacted by Dodd-Frank, too. For example, as per Section 1473, there are now minimum standardized requirements that must be followed in order for states to register AMCs. The large AMCs will be best situated going forward under these new rules.

The primary provisions of Dodd-Frank that are of concern to the mortgage industry include:

- Credit risk retention

- The Office of Credit Ratings

- The CFPB

- Coverage of mortgage lending

- Duty of care

- Prohibition of steering

- Ability to repay

- Safe harbor-qualified mortgages

- Three percent limit

- Liability of mortgage originators

- Discretionary regulatory authority

- Prepayment penalties

- Average prime offer rate

- Arbitration

- HOEPA expansion

- Appraisals, AMCs, and AVMs

- Servicing

- Counseling

- Reach of bill

- Regulatory authority

(Source: Berkery Noyes)

Traditionally, mortgage servicing lagged far behind the originations sector in terms of technological innovation. Loan origination software (LOS) businesses have long been engaged in organic innovation, as well as making acquisitions, with the goal of providing a more bundled solution. This includes product and pricing engines, CRM and automated marketing solutions, compliance tools, and e-document collaboration capabilities.

However, the servicing sector is quickly catching up on technological innovation as financial institutions become more proactive in meeting regulatory mandates. In particular, servicers are looking to improve their communications with borrowers, such as through a single point of contact, which can help reduce the number of foreclosures. There is also greater demand for frequent communications through email, text messaging, and more complex print offerings as new database technologies make it easier to compile disparate pieces of information about consumers.

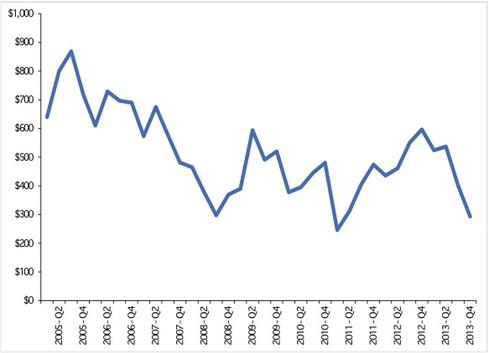

It also helps to take some historical data points into account. Since 2005, the aggregate dollar value of mortgage originations has declined.

(Source: Mortgage Bankers Association)

At the same time, the cost to service loans has been rising. Before the credit crisis, for performing loans, it would typically cost servicers an average of $55 per loan each year. The estimated cost to service a performing loan today is about $208 each year, according to a servicing operations study by Accenture. Meanwhile, certain pieces of legislation, including the Home Affordable Modification Program and the Making Home Affordable Program, are also imposing new and evolving regulatory challenges on servicers.

How might the regulatory landscape continue to impact the mortgage industry? For one thing, some credit unions may seek to outsource their compliance functions in order to focus on lending and serving their clients. Since regulations are constantly changing, it is sometimes more efficient to utilize the offerings of a mortgage technology vendor instead of creating an extensive in-house compliance department. Secondly, more stringent capital requirements and minimum reserve ratios are becoming the norm. Small institutions are not exempt from many of the regulations put forth by the Basel III standards, which could lead to an array of compliance and record keeping costs for community banks and credit unions.

Because technological growth is often followed by investments in products and companies that offer innovative solutions, third-party vendors in the mortgage servicing sector that assist with mitigating risk and strengthening compliance are well positioned to benefit.

Join the Women in Technology Panel & Luncheon at Interop on Wednesday, Oct. 1. How different are IT career paths and opportunities for men and women in 2014? Join your peers for an open forum discussing how to advance in an IT organization, keep your skills sharp, and build a mentoring network.

John Guzzo is a Managing Director at Berkery Noyes, specializing in the Financial Technology & Services group. He previously spent eleven years in investment banking and financial services at Giuliani Capital Advisors (formerly Ernst & Young Corporate Finance) and Ernst & ... View Full Bio